A mortgage is often the most significant financial obligation in a person’s life. Beyond providing a home, it also influences your financial standing, particularly your credit score. Your credit score is a vital factor that determines your ability to access future credit, such as an instant loan against shares, or invest using the best online mutual fund investment platform India. In this article, we’ll delve into how mortgages impact credit scores, both positively and negatively, and provide strategies to maintain a healthy financial balance.

1. How Mortgages Affect Credit Score

Your credit score is calculated using various factors, and your mortgage plays a role in each of these areas:

| Credit Factor | Impact of Mortgage |

| Payment History | This is the most critical component of your credit score, making up 35% of it. Timely mortgage payments demonstrate your reliability and discipline. Missing even a single payment can cause a significant drop in your score. |

| Credit Utilization | Mortgages are installment loans, so they don’t impact your credit utilization ratio the way credit cards do. This means your mortgage doesn’t hurt your utilization rate, but managing other debts alongside your mortgage is essential. |

| Length of Credit History | A long-standing mortgage can significantly enhance the average age of your credit accounts. Since credit age contributes 15% to your score, keeping your mortgage open over its term positively affects this factor. |

| Credit Mix | Having a mix of credit types, such as installment loans (mortgages) and revolving credit (credit cards), boosts your score. A mortgage enhances this diversity, showing lenders you can handle different kinds of debt responsibly. |

| New Credit Inquiries | When you apply for a mortgage, lenders perform a hard inquiry on your credit report. While this can temporarily lower your score, it’s a minor and short-term effect compared to the long-term benefits of responsible mortgage management. |

Understanding these components allows you to see how a mortgage fits into the broader context of your credit profile.

2. Immediate Impact of Getting a Mortgage

Applying for a mortgage brings some immediate changes to your credit score. Here’s what happens:

- Hard Credit Inquiries: When a lender reviews your credit report, it triggers a hard inquiry, which typically reduces your score by 5–10 points. Multiple inquiries over a short period can compound the effect. However, most credit scoring models treat multiple mortgage inquiries within 14–45 days as a single inquiry, recognizing the rate-shopping behavior.

- Increase in Debt: Taking on a mortgage increases your overall debt, impacting your debt-to-income (DTI) ratio. Although this doesn’t directly affect your credit score, lenders consider it when assessing your financial health.

Despite the initial dip, your score can recover quickly if you make timely payments and manage other debts effectively.

3. Long-Term Mortgage Benefits for Credit Score

A mortgage can be a powerful tool for building credit over the long term. Here’s why:

- Payment History: Making consistent, on-time payments demonstrates reliability, the most important factor in your credit score. Over time, this positive payment history outweighs any initial impact from hard inquiries.

- Credit Age and Stability: Mortgages typically have long terms (15–30 years). Keeping a mortgage account open contributes positively to the average age of your credit accounts, which is another critical factor in your score.

- Creditworthiness: A well-managed mortgage signals to lenders that you are a responsible borrower. This can make it easier to qualify for other financial products like instant loans against shares or personal loans at competitive rates.

By focusing on long-term benefits, you can turn your mortgage into a cornerstone of your financial stability.

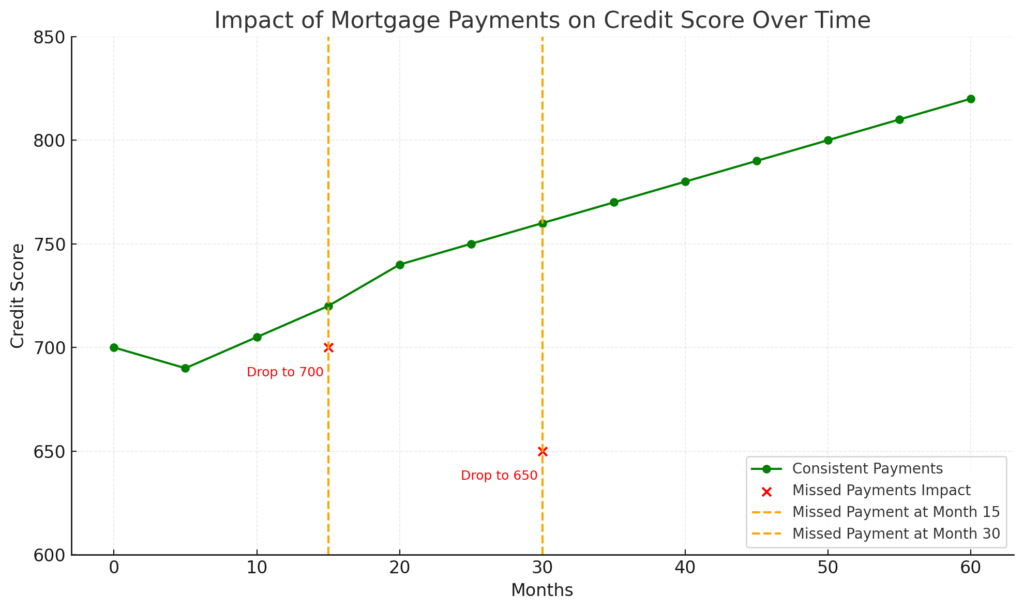

4. The Cost of Missing Mortgage Payments

Failing to make mortgage payments can severely damage your credit score. The penalties grow more severe the longer you delay:

| Days Late | Effect on Credit Score | Additional Consequences | ||

| 30 Days Late | 50–100 point drop | Late fees and notification to credit bureaus. | ||

| 60 Days Late | 100–150 point drop | Further damage to your score and risk of penalties. | ||

| 90+ Days Late | 150+ point drop | Foreclosure risk and long-term credit impact. |

Missed payments stay on your credit report for up to seven years, making it crucial to prioritize your mortgage payments.

Also Read : How to Avail Tax Benefits on Your Loan Against Property

5. Strategies to Manage Your Mortgage Effectively

To ensure your mortgage helps, rather than harms, your credit score, follow these strategies:

- Set Up Automatic Payments: Automating payments reduces the risk of missing due dates and incurring penalties.

- Budget Carefully: Allocate funds for your mortgage while leaving room for other financial commitments, such as investments through the best online mutual fund investment platform India.

- Avoid Overextending Yourself: Before taking on a mortgage, assess whether your income can comfortably cover monthly payments.

- Monitor Your Credit Regularly: Check your credit report to ensure your mortgage payments are being accurately reported.

- Leverage Financial Tools: If cash flow is tight, consider options like instant loans against shares, which can provide short-term liquidity without disrupting your financial plan.

By adopting these strategies, you can manage your mortgage effectively and maintain a healthy credit score.

6. Balancing a Mortgage with Other Financial Goals

A mortgage doesn’t have to hinder your ability to achieve other financial objectives. Here’s how to balance your commitments:

- Using Your Home Equity Wisely: If you’ve built equity in your home, you might consider a home equity loan to fund other investments or emergencies.

- Investing in Mutual Funds: Platforms like Divadhvik, the best online mutual fund investment platform India, allow you to grow wealth alongside managing your mortgage. Allocating funds smartly between repayments and investments can create a balanced financial portfolio.

- Emergency Funds: Ensure you have an emergency fund to cover unexpected expenses, so your mortgage payments remain uninterrupted.

Balancing multiple financial priorities ensures that your mortgage contributes positively to your overall financial well-being.

Conclusion

Your mortgage is a critical factor in shaping your credit score. While it may initially cause a small dip in your score, its long-term benefits outweigh the short-term impact—provided you manage it responsibly. Timely payments, careful financial planning, and leveraging tools like instant loans against shares or mutual fund platforms such as Divadhvik can help you maintain financial stability and achieve your goals.

Ultimately, understanding how a mortgage fits into your broader credit and financial strategy is key to maximizing its benefits. With proper management, you can enhance your credit score, secure your home, and create a pathway to long-term financial success.